Scottish Liberal Democrat leader Willie Rennie has been taking a bit of a pasting on social media from nationalists who don’t like what he said in a tv interview yesterday. He argued what I thought was a pretty obvious point that in a Scotland where we were using the pound without the protection of a lender of last resort and where Alex Salmond had led us to inglorious default on our share of the UK debt, our mortgages, car loans and credit cards would be more expensive than they are now.

There are several reasons for this. First of all, if we have no lender of last resort, the banks have to keep more money in their reserves which mens they have less to lend out. That will push up their interest rates to start with. We would all end up paying more. Think about the effects that would have on already stressed household budgets. We’ve so far avoided the huge spike in repossessions that we saw in the 1990s recession. That could change rapidly.

Remember when Vince Cable was complaining that viable businesses were really struggling because banks wouldn’t lend to them in the wake of the last recession? We’d have that to deal with as well.

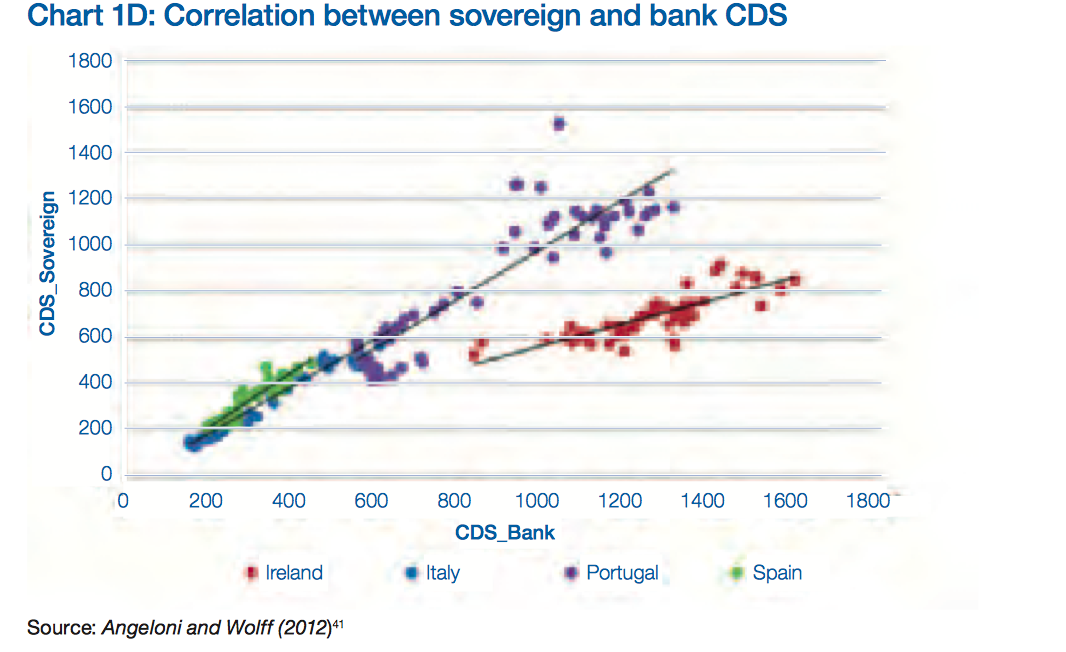

Yes campaigners would have us believe that Government borrowing rates and consumer borrowing rates were completely unrelated, yet there is evidence that there is a correlation between the two. I might find an economic system in which the interest I pay is based on whether some rich blokes (and they usually are blokes) are feeling confident or not bizarre, but that’s the way it is and the global economic system is hardly likely to change just because Scotland gets its independence. The Scotland’s Office Scotland Analysis paper on the Financial Services Industry shows that if the money markets don’t have confidence in a government, they won’t have confidence in the banks in that country either. Both Government and banks therefore end up paying higher interest rates. The paper says:

As a number of independent commentators have argued, if Scotland became independent it would not have the UK’s track record with the international financial markets, and could therefore be perceived by financial markets as less credible. When markets perceive weaknesses in the credibility of the sovereign, this negatively impacts the credibility of domestic banks, with a consequent increase in the cost of funding. Market perceptions of banks’ solvency are more closely linked to perceptions of the sovereign during periods of stress, particularly for those countries that experience a significant deterioration in their sovereign credit risk.

They have a model which shows the correlation:

So if the money markets take a dim view of Scotland because of the make-up of our economy or because we’ve defaulted on our debts, we will suffer twice. First of all, the higher cost of borrowing will mean that the government can fund fewer public services. Secondly, we’ll all be paying more than we are now for our personal credit in whichever form it comes. It’s not pretty.

Of course, the Yes campaign, and Alex Salmond himself, will argue that it’s the UK’s debt, not Scotland’s, legally, because the UK has guaranteed it. Why is that the case? Because it had to when the markets got spooked earlier this year. They were worried about lending to the UK and then facing the prospect of having to chase Alex Salmond for 10% of it after he originally threatened that he wouldn’t take a share of the debt. So the legal guarantee he is going on about is only there because of his irresponsibility. As his own trusted adviser Crawford Beveridge said last week, even if it technically isn’t a default, if it looks like Scotland isn’t taking on its debts, then the markets will react accordingly.

In addition to all of that, research by Costas Milas from Liverpool University and Tim Worrall of Eidnburgh University showed that even the Yes campaign rising in the opinion polls before a vote was cast made the markets more hesitant and unwilling to borrow over the longer term:

Our results suggest that a 12 percentage point increase in the Yes rating relative to the No rating lifts the 10-year borrowing costs relative to the 5- year borrowing costs by up to 24 basis points; it also rises with the size of the Yes_lead poll result.

Earlier this year the Money Marketing website looked at how mortgage lenders would review their lending in the event of a No vote.

Precise managing director Alan Cleary says there is uncertainty over currency, house prices and mortgage availability and lenders would be “nuts” not to launch a review following any yes vote.

He says: “There is a whole bunch of stuff we would have to review to make ourselves comfortable we could still confidently lend in Scotland. It will be the case for everyone and lenders would be nuts not to do it.”

Of course on top of all of this added cost of borrowing, Scots would face the loss of a significant guarantee in the event of a banking crisis. Our savings are protected by the UK up to £85,000 which is more than enough for most uf us. If our banks went under, we’d get that money back. That would not be the case in an independent Scotland using sterling outside a currency union.

Willie Rennie had this to say on the uncertainties of the currency plans:

The Yes campaign is involved in a conspiracy of silence to hide the real impact of their independence plans on Scottish households. With billions of pounds of consumer debt in Scotland any increase in interest rates would hit households hard in their pockets. But that’s exactly what will happen if Alex Salmond refuses to pay Scotland’s fair share of national debt.

A default of government debts on the first day of independence will put borrowing costs for the Scottish Government up. The international markets will charge them premium rates as the risks will be judged higher.

The contamination caused by a Scottish default would directly infect consumers in Scotland.

Figures from the Council of Mortgage Lenders suggest that households in Scotland owe £100 billion on their mortgages. With billions more tied up in other consumer loans any increase in interest rates would hit consumers hard in their pockets.

That’s the consequence of Alex Salmond’s plans. As part of the UK Scotland has a solid reputation for sound money across the globe. Refusing to pay our share of public debt will trash that reputation in just one day.

Alex Salmond’s refusal to deny that consumer debt costs would rise if he turned his back on Scotland’s fair share of public debt is revealing in itself. There is a conspiracy of silence at the heart of the Yes campaign. They know that their reckless threat to effectively default would cost consumers millions of pounds. Alex Salmond should speak out on this matter. He must not be allowed to let this be another unanswered question on the cost of independence.

His Fiscal Commission chairman Crawford Beveridge confirmed that walking away from Scotland’s fair share of debt would be the equivalent of a default. And a default sends warning signals to investors who subsequently want a higher price for investing in those bonds as a result of the higher risk.

The National Institute of Economic and Social Research have predicted that borrowing costs in an independent Scotland could go up by 1-2%. Translated into mortgage repayments, it could mean a rise of £1,300 per year for a 75% mortgage. And credit cards could go up by £120. Alex Salmond’s reckless default threat will hit us hard in our pockets.

Alex Salmond’s default threats make life in post independence Scotland a whole lot riskier.

* Caron Lindsay is Editor of Liberal Democrat Voice and blogs at Caron's Musings. You can find her on Bluesky at caronmlindsay.bsky.social

17 Comments

First, it’s questionable that it would amount to “default”. It’s the UK’s central bank’s debt, so if Scotland is denied any share in the UK central bank, it has no obligation to share its debt.

Even if it were thought immoral of Scotland not to offer to share the debt, international financiers are not moral agents. They would take a cold look at Scotland’s finances, and set interest rates accordingly. A debt-free Scotland could well attract lower interest rates than rUK.

Of course the situation is uncertain, and of course the Scottish government may be wearing rose-tinted spectacles, but the uncertainty is largely due to the UK government’s adopting political postures rather than discussing (as the Edinburgh agreement suggests they should) what currency arrangements would work best for both countries.

We will only get sensible currency discussions when and if there’s a Yes vote.

It’s worse than that. Economic theory would say pretty unambigiously that mortgage rates to new Scottish mortgage borrowers will go up on September 19th in the event of a ‘yes’ vote since the security of any mortgage loan (i.e. the property) is, for most of the repayment period, set to be in a country with less clear and more risky financial arrangements than the equivalent loan in the UK. When the markets know that something is definitely coming or that uncertainty is definitely coming, they don’t wait, but price for it immediately. In practice – because people only have a certain amount of disposable income for housing – this could even mean an immediate and sharp drop in Scottish house prices – although market sentiment could override that…

@Denis – because the perception of greater risk of sovereign default has worked out so well for everyone else? http://en.wikipedia.org/wiki/List_of_sovereign_debt_crises This isn’t about the law, it’s about risk. And there is no seriously imaginable way in which risk will be perceived to be lower on loans to Scottish individuals and companies in the event of a ‘yes’ vote on September 18.

It is about risk. But, we are in 2014, not 2008. Earlier this year, the mere suggestion that the European Central Bank was willing to guarantee the liquidity of the major Bulgarian banks staved off a run on those banks and prevented another Greece in the Balkans.

There is no really credible reason why the European Union would not extend the same coverage to Scotland, even in the highly unlikely scenario of it not making an uninterrupted transition to full member-statehood.

Of course Scotland would find a factor of additional risk added to the cost of borrowing at every level. But I think you will find that it will be minimal, and will quickly readjust to a perfectly reasonable level as full confidence returns.

A Scottish default would surely hurt the rUK pound, because the rUK’s debt-to-GDP ratio would go up, making it harder for rUK to pay back the national debt, probably meaning further and longer austerity.

rUK’s electorate is unlikely to be happy about this. It could damage relations between rUK and Scotland badly, making other aspects of settlement more difficult to agree and less likely to favour Scotland. It would likely reduce the willingness of rUK’s consumers to buy Scottish goods and services. The reduction in foreign income would be a further factor in reducing confidence in Scotland’s ability to repay future loans.

In short, a Scottish default would damage everybody.

As for the EU bailing out Scotland, that would only happen if Scotland came near to crashing its financial system, and it would put Scotland in the Greek category. It’s hardly an argument in favour of debt default!

“Don’t think. Don’t bother with the details. You don’t have time to research the arguments; you are too busy, and there’s not enough time, and there are more important things for you to do. Don’t worry your head about anything. Just give us your vote, and we’ll take care of things. Vote no in the independence referendum in Scotland. If you think and choose what wwe don’t want ou to choose, it will be bad for you.”

In essence this is the case for the union delivered by the Better Together campaign in Scotland. I have followed it, more or less disinteredly over the last few weeks or months. Days go by without me thinking about it because, let’s face it, it is far away from me and I don’t have a vote. Then I realise that the effects of the vote will impact me, and I binge for a few hours and try to catch up.

Both The Times, The Sun and The Daily Mail now scream that the Union hangs in the balance. The polls have narrowed so much that they are, basically, operating within the margin or error territory that can be called ‘the statistical dead-heat’. Today, YouGov published that there was a six per cent gap between Yes and No in the referendum. With a 3 per cent margin or error, the polls can land anywhere. It is the third poll which shows a large movement from No and Undecided toward Yes. Declarations that “it is a foregone concluson” sound hollow, laughable, now.

But would not the reason for that arise from the main angle of the Better Together campaign? They have not made a case for the union. Their vision is that politics is too difficult and too exhausting, and the voters should just vote No and leave political thought to the politicians. Is this not the reason why there is such voter apathy in the electorate, because the voters have believed this?

If I were Scots, this message would be deeply offensive to me. At least when stated so clearly in an actual campaign. But is this not the unstaded message in all campaigns? Is this not the default statement of any election within the United Kingdom? Don’t think. We know what we’re doing. Don’t look around in your life and aspire for something better. Whatever you want will be bad for you. Don’t think. Don’t choose. Don’t worry. Trust us.

I certainly envy the Scots. They seem to have found their democratic soul, and look set to deliver a blow against austerity and neoliberalism in these isles. The first such blow in thirty years. If the result comes back as yes, and that looks more and more likely, it will be a death’s bell tolling for the Westminster model of parliamentary democracy. And it’s not a day too soon.

I accept I may be wrong but Scotland wishes a share of assets if they decide in favour of independence surely if they do not wish through the representative they say we won’t pay the national debt to rUK rUK can say part of your settlement is the pensions bill

So no share of national debt the Scottish parliament makes its debt payment direct to its electorate over many years

I don’t mean tit for tat just they should be persuaded to pay one way or the other more so as their argument is they are Very rich

I think this could all get very messy, very quickly and whatever the Scots like to think, in the event of Yes vote the biggest consequences are likely to be the north of the border.

The trouble is, the referendum is very cannily being turned by Salmond into a vote on whether the Scots like (1) the realities of austerity; (2) the Coalition government; (3) the English, particularly posh ones and particularly Cameron.

Meanwhile, on bread and butter issues, rhetoric is gaining ascendancy over reasoning. Precise understanding of the technicalities of what would actually happen in the even of Scotland reneging on its debt commitments as part of the UK among the wider voter base is obviously lacking. Witness the comment by Denis Mollison above:

“First, it’s questionable that it would amount to “default”. It’s the UK’s central bank’s debt, so if Scotland is denied any share in the UK central bank, it has no obligation to share its debt.”

The national debt is the government’s debt, not the central bank’s debt. And the idea that Scotland can be given a “share” of the Bank of England, the central bank of what would be a sovereign foreign nation (the UK) in the event of Scotland voting for independence, is clearly not even remotely feasible.

It is this inability to accept clear, undisputed facts and the insistence on reinventing reality around how they would like things to be that is most worrying about the Nats. They are wandering off into fantasy land and unfortunately many voters are disposed to believe them because the alternative, the hard truth of the real world, is too difficult to deal with.

“Don’t think. Don’t bother with the details. You don’t have time to research the arguments; you are too busy, and there’s not enough time, and there are more important things for you to do. Don’t worry your head about anything. Just give us your vote, and we’ll take care of things.”

Isn’t that the Yes campaign?

The degree of inter dependence such as how much of the pensions system works means that it is virtually inconceivable that that there would not be some kind of shared currency agreement, no matter what Danny Alexander, Alistair Darling and George Osborne say.

However on the narrow debt issue, talk of a default is nonsense. The debt is a B of E debt, if the B of E is not shared then the only debt is one that Scotland agrees to take on. No lender would turn to Scotland for repayment since they have no agreement with Scotland. Of course rUK could refuse to pay 100% of loans, leading to a rUK default that then might knock on to Scotland. There is no mechanism whereby Scotland could default on this debt, without rUK defaulting as well. Even in such an unlikely eventuality, I do not think that technically it could be a default for Scotland.

The more important point is that this is the type and tone of discussion that will poison the aftermath to the referendum.

There is an irony in all this. If Scotland votes Yes , that could be the salvation of the English and Welsh Liberal Democrats.

England usually has a Conservative majority, against that background and with a Conservative government in England and Wales the Lib Dems would probably prosper against an unpopular government and could in the longer term pass Labour as the left, left of center opposition, in England anyway. Give the Welsh their independence and we could be well away.

Technicalities about which institution holds the debt are irrelevant. The debt was acquired by the whole of the UK. It’s pretty certain sure there will be serious repercussions if Scotland refuses to pay its share and saddles every taxpayer in rUK with an additional £3000 or so to pay on its behalf. Politicians in rUK would need someone to blame.

The whole issue illustrates Salmond’s ignorance in financial matters and as regards what will become part of Scotland’s foreign policy if Yes wins. It’s a pretty clear indication that Yes will mean Scotland going down the tubes in its first few years at least.

In the longer term, like everyone else, Scottish people are likely to find that sharp borders are a marked disbenefit in a modern, highly connected world, and complete “independence” is neither desirable nor possible for anyone.

There’s no Tory majority in England, it’s a myth. If it is a Yes vote then the obvious explanation will not be that the Scots believe in Salmond’s land of milk and honey (more still expect to be worse off post-independence than better off) but a rejection ‘Tory’ Britain. The vast majority of Scots simply have no affinity for the Party of Cameron, Osborne and Duncan Smith.

The irony is that the Tories haven’t won an election in over 20 years and don’t look like winning one soon. The y have of course been able to govern at a UK level for the last 4 years thanks to the goodwill of another Party who were happy to implement a broadly Tory agenda. Just look at the Yes campaign placards – no more bedroom tax, saving the NHS etc. And look at where they are gaining support. Labour and Lib Dem voters in the central belt.

Let’s concentrate our fire on the YES campaign’s weakest point: ask the big £85000 question concerning bank account protection. Here it is: how can an independent Scotland without a lender of last resort guarantee bank accounts the same way the British government does? It can’t.

Alec Salmond and Nicola Sturgeon sidestepped this question at Holyrood. Let’s make it the BIG QUESTION of the remaining part of this campaign. Never mind detailed economic arguments containing many points. Ask the big £85000 question which has a very real meaning for everyone in Scotland. Aim to erode the weaker part of the support for YES. Make people realise the SNP have got no answer. Make them think of this when they’re on their way to vote.

Denis

“First, it’s questionable that it would amount to “default”. It’s the UK’s central bank’s debt,”

Firstly it is UK government debt not BoE debt.

The position would be the Scottish government was partially responsible for running up the debts so the borrowing was on their behalf by the UK govt. The remaining intra-government liability will stand and it is that which is being defaulted on. Your statement suggests is one that suggests that UK debt would be rede nominated as owed by Scotland, that is not the case. To an outside observer the Scottish government ran up a debt and failed to pay it that is a default. It doesn’t matter if you default on publicly traded debt or if you default on Intra-government debt, you default.

A future lender may think the default is unique (they always are you know)

“so if Scotland is denied any share in the UK central bank, it has no obligation to share its debt.”

No one has suggested that in. The event of a yes vote if the Scottish government want a tiny minority share of the BoE they can’t have it they just can’t use a currency backed by the rUK tax payer.

You also appear to misunderstand currency is a liability not an asset, don’t believe Salmon’s rhetoric it is not an asset.

“Even if it were thought immoral of Scotland not to offer to share the debt, international financiers are not moral agents. They would take a cold look at Scotland’s finances, and set interest rates accordingly. A debt-free Scotland could well attract lower interest rates than rUK.”

Who said anything about morality, bond raters are not interested if you beat your wife, kill your population or destroy the planet. They care about the risk you won’t repay. And an important factor is if it is if your population is likely to vote in governments who are likely to try and wriggle out of their obligations, just ask Argentina. Of course the Scottish government could borrow in US dollars under Ny law and get a good rate but that carries risks.

Richard

“A Scottish default would surely hurt the rUK pound, because the rUK’s debt-to-GDP ratio would go up, making”

The liability side would be unaffected so the debt to GDP ratio (it will rise in the event of a split regardless) would be in affected, it would be a write down in assets so there would be an increase in risk so borrowing costs would rise but the ration would not be affected depending not the decision.

Martin

“The debt is a B of E debt”

UK debt is issued by the UK debt management office not the Bank of England.